Summer 2017

With the exception of a few recent instances of increased volatility, the equity markets have been quite calm in the past few months. This steadiness has persisted despite the Syrian war and refugee crisis, Brexit, terrorist attacks in Europe, the U.S. election and its political aftermath, the North Korean nuclear threat, and other global events.

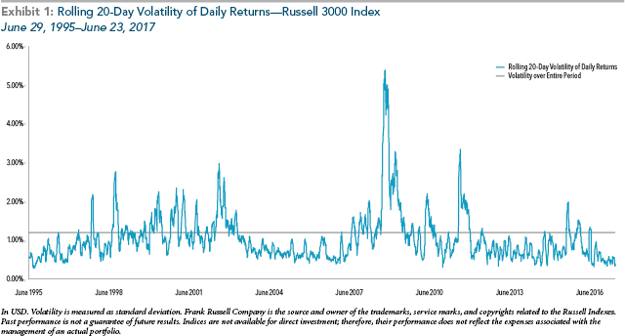

Exhibit 1 shows the rolling 20-day1 volatility of daily returns of the Russell 3000 Index since 1995. Currently, volatility has fallen below its standard deviation for the entire period—an indication that the U.S. equity market volatility has been low.

There has been much speculation in the press about why volatility has been low, how this is related to the real economy and global events, and what it might mean for future returns. However, these are just stories. Whatever is underpinning the lack of volatility might not matter much anyway, as research shows that volatility does not indicate whether future returns will be high or low.2

Today’s level of volatility will not tell us when, why, or by how much the market may drop, because volatility often spikes during a market decline.2 Instead of dwelling on the unknowable, we should focus on what we do know: Over time, stock markets have been volatile, but their long-term returns are much higher than those for cash or bonds. Investing in the markets is the best way to beat inflation, too.

Clients should not be caught off guard by the next market downturn, whenever that might occur—it will happen, we just don’t know when.

Keep Calm & Carry On…Even in Downturns

History has shown that volatility spikes and market downturns can happen unexpectedly. This is why it is important to develop an appropriate asset allocation and to set reasonable expectations that can help you weather market downturns.

Investors vary in their ability to bear volatility. Those with little appetite or ability to experience declining portfolio values dampen volatility with bonds. During periods when equity markets fall, a well-designed allocation to fixed income can help mitigate the declines experienced at the overall portfolio level.

If you’re a veteran of one or more turbulent markets, it may still be difficult to maintain discipline in the future, especially if you are close to or in retirement. Even though past experiences can inform our future actions, falling stock prices typically come with a litany of bad news and the stress of not knowing when the downturn will end, which can cloud memories and tempt investors to assume that “this time it’s different.”

Also, it’s important to note the difference between a realized loss and a drop in prices. Global markets have historically recovered from a price drop. However, investors who get out of the market when prices are low lock in their losses. Buy low, sell high is the winning formula.

Stocks Rise & Fall, but Markets Go Up (Over Time)

Stock prices can and do fall, but global markets are resilient. Exhibit 2 shows how a hypothetical 100% equity strategy and a hypothetical 60% stock/40% bond strategy would have fared in the past six global stock market downturns of at least 20%. On average, a decline of this magnitude has occurred about once every seven or eight years since 1973. The last occurrence was in 2011. The addition of bonds would have helped to mitigate the decline in the 60/40 strategy relative to 100% equity strategy. Additionally, investors might take comfort in knowing that for most of the historical downturns, $1 invested in either strategy at the market high point (before the decline) would have resulted in positive growth within both 5 and 10 year periods.

No Risk, No Reward

If investment outcomes were certain and prices never declined, we would not expect much return. For many investors, the expected return of cash and short-term Treasuries is not sufficient to meet their long-term financial goals. In a world of stable portfolio values, investors would end up trading one risk (volatility) for another risk—loss of purchasing power after taxes and inflation from investing only in short-term Treasuries.

Framed in this way, uncertainty and market declines are part of the nature of investing. Uncertainty is not a pleasant experience for most investors—and market downturns can bring discomfort. But learning to embrace their inevitability can be liberating. While not trying to induce unnecessary anxiety or leave the impression we are predicting that another market decline is imminent, it’s never too early to revisit your investment expectations. Please let us know if you have concerns about your portfolio allocation so that we can discuss potential solutions.

- We use 20 days as an approximation for the number of trading days in a month.

- “Can Volatility Predict Returns?” (Issue Brief, Dimensional Fund Advisors, July 2016).

This article was adapted from “Complacency and Calm Markets” by Brad Steiman, Dimensional, published June 30, 2017.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

This article is distributed for educational and informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, product, or services.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions.