At JLFranklin Wealth Planning, we are healthy and physical distancing while doing our best to comply with the State of California’s Stay-at-Home order. Fortunately, Zoom video conferencing allows our team to meet daily, and it’s also how we meet with clients.

Two events are occurring simultaneously: The COVID-19 pandemic and the stock market’s reaction to it. We encourage you to separate the two by taking action to protect your health, and resisting the temptation to take hasty action when it comes to your portfolio. Staying in the market is the best way to achieve your goals. Selling out now, after a big drop, is the best way to ensure that you’ll need to work longer, possibly postponing retirement by years.

What Clients Are Asking

Lately, I’ve been spending a big chunk of my day responding to client email and phone calls. Below are some questions I’ve gotten about the recent market drop.

Given the unprecedented health crisis, should we sell, take our losses, and then re-enter the stock market once it has bottomed out?

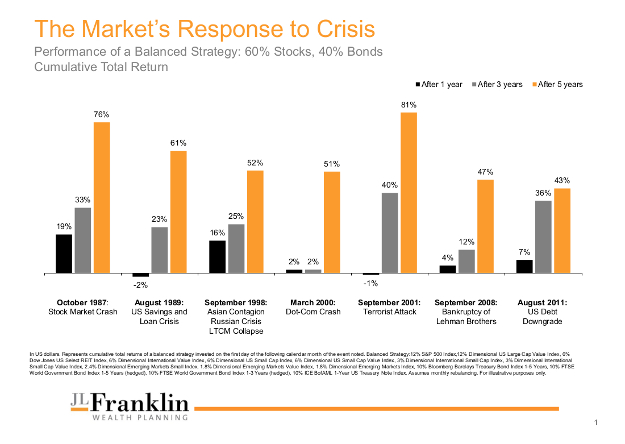

As one Wall Street saying puts it, “They don’t ring a bell at the bottom.” The strongest argument for remaining fully committed to your investment allocation is the historical performance of stocks after the type of decline we have already experienced, illustrated in this chart, “The Market’s Response to Crisis.”

When markets recover, they move quickly. Early returns are often huge, and any paper losses sustained during the downturn will not be permanent as long as you do not cash out. Over the next few months, numerous variables could push the global market either way. No one knows with confidence which direction the financial markets are headed in the short term. However, the assets you have invested in stocks and bonds are those you anticipate that you will not need for living expenses for at least five years. We are confident that our approach of highly disciplined, rational allocation, coupled with the patience to let it work, will reward clients over the long term.

When will my portfolio rebound?

Although we are not confident in assessing the outcome for the economy over the next year, whatever the economic scenario, over the long term the economy will expand, and this will lead to corporate earnings growth that will drive stock prices higher. During bear markets, investors are more likely to make decisions based on fear. We strongly discourage emotionally charged investing.

When stocks are undervalued, does this mean the market will rebound soon?

Not necessarily. As long as fear is dominant, investors will demand a high-risk premium (lower price/earnings multiple). So, how long the fear factor lasts is the key to shorter-term market performance.

If we are in a recession, why not avoid stocks until things settle down?

By the time things settle down (if such a time can be easily identified), stocks will have already moved significantly higher. The collective actions of investors are driven by anticipation of what will happen in the future, and why stocks have been falling for weeks. Investors anticipated the earnings slowdown from COVID-19 and now are discounting a further earnings decline. Stock prices reflect a new bull market prior to the end of recessions—usually three to nine months before the economy bottoms. And it is also why stocks always bottom when the outlook is most dire, since after that point things can only get better. Identifying the exact point of maximum pessimism is impossible.

I have a dollar cost average strategy in place. Should I stop investing and wait for the market to stabilize?

Financial markets anticipate the future; the time to buy is often when the outlook is particularly grim. In the past, buying during a recession has almost always been a great strategy.

When I look at my holdings on Schwab.com, why does the value not change during the day?

Many of your holdings are invested in mutual funds which are priced once per day, at market close. You won’t see intra-day price changes for these holdings. Instead, their prices will be adjusted after market-close which is 1 p.m., Pacific Time.

Are my assets protected at Schwab?

The brochure How client assets are protected at Schwab provides an overview of asset safety and insurance policies. To learn more about Schwab’s stability, review additional information about the Schwab Corporation.

With interest rates so low, should I refinance my mortgage?

Maybe. Contact Quicken Loans, which is owned by Schwab Bank. Feel free to reach out to advisor client rep Veronica Rubio at Veronica.Rubio@Schwab.com or (415) 849-8349.

What We Are Doing for Clients

We are reviewing all taxable accounts to harvest tax losses. This powerful wealth-creating strategy requires analysis and careful review of all holdings to avoid the “wash sale rule” that says you can’t take a loss if you’ve purchased a security in any account within 30 days before or after the trade (including reinvested dividends). Our work will protect you in the event of a tax return audit.

Additionally, we are rebalancing all portfolios back to asset class targets, so you buy low and sell high.

Tax Day Deferred

As part of the federal government’s relief program during the COVID-19 pandemic, federal income tax filing and payment deadlines are postponed. Instead of filing and paying on April 15, you have until July 15. The 90-day extension also includes self-employment tax of sole proprietors and the first quarterly estimated income tax payment for 2020, normally due April 15.

Per the Franchise Tax Board, California has extended the file and pay deadlines from April 15 to July 15, 2020. If you live in a state other than California, check your state tax agency’s website for any changes to filing or payment dates.

Summary

It is easy to find plenty of intelligent-sounding predictions about the economy. Investors are drawn to such forecasts because they make investment decisions easier. Unfortunately, accurately predicting the future is another story. The real key is to accept that some things are inherently uncertain and instead focus on the knowable.

All clients have gone through a risk coaching discussion to balance risk tolerance, time horizon, and overall investment objectives. If you would like to review the appropriateness of your cash flow or investment strategy, please let us know; however, if it appears a reduced-risk strategy is appropriate, it is likely best to implement a change after the market rebounds.

We remain strongly committed to helping you achieve your goals by protecting your assets.