Fall 2018

To say that “money isn’t everything” is beyond cliché. Studies in the early 1970s demonstrated that a sense of well-being, or happiness, had not increased commensurately with income over the previous half century.1

That trend continues, as the modern world has arguably made well-being more elusive than ever. Since the 1990s, the positive psychology movement has attempted to find the key to understanding what makes people flourish. It has spawned the so-called happiness literature that seeks modern truth by weaving together science and ancient wisdom. How to be happier is now the most popular course at Harvard and Yale.2

Businesspeople and entrepreneurs are also contemplating some of these age-old questions. Mo Gawdat, a serial entrepreneur and former Chief Business Officer at Google X, tried to engineer a path to joy in his book, Solve for Happy, by expressing happiness as the following equation:

HAPPINESS ≥ Your perception of the EVENTS of your life − Your EXPECTATIONS of how life should behave

According to Gawdat’s model, if you perceive events as equal to or greater than your expectations, then you’re happy – or at least not unhappy.

Investors wanting to increase their wealth and well-being should consider his model. You can’t control most events that affect your portfolio, but events themselves are not part of the equation. Fortunately, you have some control over the two variables driving happiness: your perception of the events and your expectations.

EXPECTATIONS

First, let’s review some fundamentals about expectations.

-

Stocks have higher expected returns than safer investments, like Treasury bills.

It is widely known that stocks are riskier, thus prices should reflect that information, and higher expected returns incentivize investors to bear that risk. The higher expected return for stocks is known as the equity premium and, historically it has been about 8% annually in the U.S.3 - All stocks don’t have the same expected return.

The price of a good or service is set by market forces and results from many factors, such as the costs of raw materials, labor, shipping, and advertising, as well as competition and perceived value. Consumers don’t need to understand all the inputs to make an informed purchase. You look at the price relative to alternatives in the market and ask if the product is worth the price; the lower the price or the more you get, either in quality or quantity, the better the purchase.Similarly, a stock’s price has many inputs. Expectations about future profits, different types of risk, and investor preferences are just a few. All available information should already be reflected in the price. Both consumers and investors want to pay less and receive more.

Therefore, expected returns are a function of the price you pay and cash flows you expect to receive. Companies that are smaller (known as “small cap”) and more profitable, with lower relative prices (known as “value”), have higher expected returns than those that are larger and less profitable, with high relative prices. These patterns are referred to as size, value, and profitability premiums. These premiums have historically ranged from slightly more than 3.5% to just under 5% in the U.S.4

- Expected premiums are positive but not guaranteed.

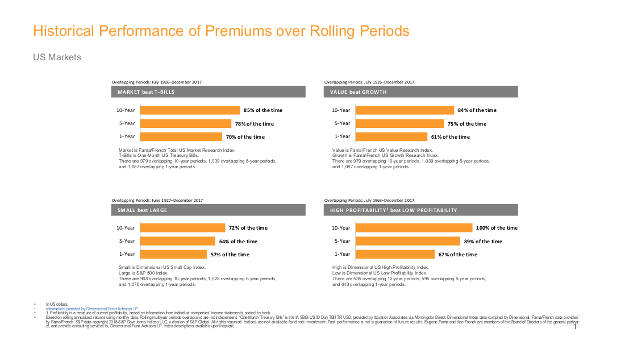

Although expected premiums are always positive, realized premiums may be positive in some years and negative in others. It’s possible – even likely – you may experience a negative premium for several years in a row. The following graph illustrates that the probability of a positive small cap premium over one year is only slightly more than a coin flip, and it is 70% for the equity premium.

The probability of earning a positive premium increases with your time horizon, but it isn’t a sure thing since underperformance is possible over any time frame. Nobel laureate Paul Samuelson said, “In competitive markets there is a buyer for every seller. If one could be sure that a price will rise, it would have already risen.”

PERCEPTION

The other half of the happiness equation is your perception of an event.

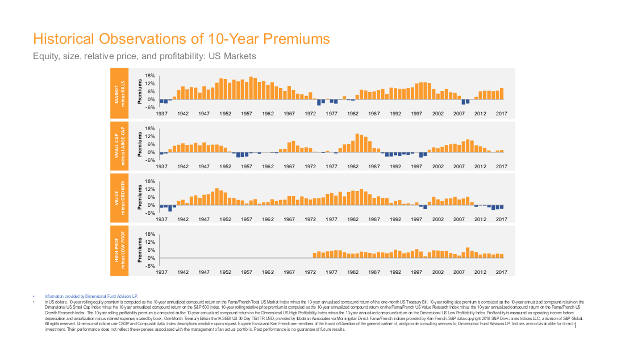

Consider underperforming a benchmark over 10 years, a time frame that some investors consider long term. This is not just a hypothetical exercise, because, as shown in the following graphic, the cumulative value premium has been negative for the past 10 years in the U.S., while the market and small cap premiums were negative in the 10-year periods ending in 2009 and 1999, respectively.

Nonetheless, disappointment from lengthy periods of underperformance shouldn’t turn into anger or regret if you know in advance that periods like these will occur and you recognize that you can’t predict them.

Ancient wisdom teaches acceptance, as resistance often fuels anxiety. Instead of resisting periods of underperformance, which might cause you to abandon a well-designed investment plan, try to lean into the outcome. Embrace it by considering that if positive premiums were absolutely certain, you shouldn’t expect those premiums to materialize going forward. Why? Because in a well-functioning capital market, competition would drive down expected returns to the levels of other low-risk investments, such as short-term Treasury bills. Risk and return are related.

The good news is there are sensible and empirically sound ways to increase expected returns. The bad news is there will be periods of underperformance along the way.

Your happiness as an investor depends on how your perception of events stacks up against your expectations. Proper expectations along with the appropriate perception can help you stay the course and may improve your overall wealth and well-being.

As always, let us know if you have questions about your portfolio or your financial plan.

Source: Adapted from Dimensional

Footnotes

- In his seminal article, Easterlin (1974) saw that while industrialized countries had experienced phenomenal economic growth over the past 50 years, there had been no corresponding rise in the happiness of their citizens. Easterlin, Richard A. “Does Economic Growth Improve the Human Lot? Some Empirical Evidence,” University of Pennsylvania, 1974.

- Ben-Shahar, Tal. Happier: Learn the Secrets of Daily Joy and Lasting Fulfillment. “Yale’s Most Popular Class Ever: Happiness,” The New York Times, 26 Jan. 2018 https://www.nytimes.com/2018/01/26/nyregion/at-yale-class-on-happiness-draws-huge-crowd-laurie-santos.html

- The market return (equity premium) from 1928-2017 was 8.27%, in U.S. dollars. Asset class filters were applied to data retroactively and with the benefit of hindsight. Actual returns may vary. Equity premium is the arithmetic average of the annual Fama/French Total U.S. Market Index returns minus the annual one-month U.S. Treasury bills returns. See Disclosures and Index Descriptions, below, for additional important information and descriptions of indices used. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is no guarantee of future results.

- Company size (small cap) premium 1928-2017 is 4.08%, relative price (value) premium 1928-2017 is 4.92%, and profitability premium 1964-2017 is 3.57%, all in U.S. dollars. Asset class filters were applied to data retroactively and with the benefit of hindsight. Actual returns may vary. Relative price is measured by the price-to-book ratio; value stocks are those with lower price-to-book ratios. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Premiums are calculated as the arithmetic average of the annual return differences between indices. Small cap premium: Dimensional U.S. Small Cap Index minus S&P 500 Index. Value premium: Fama/French U.S. value minus Fama/French US. Growth Research Indices. Profitability premium: Dimensional U.S. High Profitability minus Dimensional US Low Profitability Indices. See Disclosures and Index Descriptions, below, for additional important information and descriptions of indices used. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is no guarantee of future results.

DISCLOSURES AND INDEX DESCRIPTIONS

Additional Disclosures for Expectations Exhibit Small cap premium is the arithmetic average of the annual Dimensional US Small Cap Index returns minus the annual S&P 500 Index returns. Value premium is the arithmetic average of the annual Fama/French US Value Research Index returns minus the annual Fama/French US Growth Research Index returns. Profitability premium is the arithmetic average of the annual Dimensional US High Profitability Index returns minus the annual Dimensional US Low Profitability Index returns. Dimensional indices use CRSP and Compustat data. Fama/French indices provided by Ken French. S&P data © 2018 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

Additional Disclosures for Historical Performance of Premiums over Rolling Periods Market Outperforms Bills: Fama/French Total US Market Index vs. one-month US Treasury bills. Small Caps Outperform Large Caps: Dimensional US Small Cap Index vs. S&P 500 Index. Value Outperforms Growth: Fama/French US Value Research Index vs. Fama/French US Growth Research Index. High Prof Outperforms Low Prof: Dimensional US High Profitability Index vs. Dimensional US Low Profitability Index. S&P data © 2018 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

Additional Disclosures for Historical Observations of 10-Year Premiums 10-year rolling equity premium is computed as the 10_year annualized compound return on the Fama/French Total US Market Index minus the 10-year annualized compound return of the one-month US Treasury bill. 10-year rolling size premium is computed as the 10_year annualized compound return on the Dimensional US Small Cap Index minus the 10-year annualized compound return on the S&P 500 Index. 10-year rolling relative price premium is computed as the 10-year annualized compound return on the Fama/French US Value Research Index minus the 10-year annualized compound return on the Fama/French US Growth Research Index. The 10-year rolling profitability premium is computed as the 10-year annualized compound return on the Dimensional US High Profitability Index minus the 10-year annualized compound return on the Dimensional US Low Profitability Index. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. One-month Treasury bills is the IA SBBI US 30 Day TBill TR USD, provided by Ibbotson Associates via Morningstar Direct. Fama/French indices provided by Ken French. S&P data © 2018 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Dimensional indices use CRSP and Compustat data.

Index Descriptions

Dimensional US Small Cap Index was created by Dimensional in March 2007 and is compiled by Dimensional. It represents a market-capitalization-weighted index of securities of the smallest US companies whose market capitalization falls in the lowest 8% of the total market capitalization of the Eligible Market. The Eligible Market is composed of securities of US companies traded on the NYSE, NYSE MKT (formerly AMEX), and Nasdaq Global Market. Exclusions: Non-US companies, REITs, UITs, and investment companies. From January 1975 to the present, the index also excludes companies with the lowest profitability and highest relative price within the small cap universe. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Source: CRSP and Compustat. The index monthly returns are computed as the simple average of the monthly returns of 12 sub-indices, each one reconstituted once a year at the end of a different month of the year. The calculation methodology for the Dimensional US Small Cap Index was amended on January 1, 2014, to include profitability as a factor in selecting securities for inclusion in the index.

Dimensional US High Profitability Index was created by Dimensional in January 2014 and represents an index consisting of US companies. It is compiled by Dimensional. Dimensional sorts stocks into three profitability groups from high to low. Each group represents one-third of the market capitalization. Similarly, stocks are sorted into three relative price groups. The intersections of the three profitability groups and the three relative price groups yield nine subgroups formed on profitability and relative price. The index represents the average return of the three high-profitability subgroups. It is rebalanced twice per year. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Source: CRSP and Compustat.

Dimensional US Low Profitability Index was created by Dimensional in January 2014 and represents an index consisting of US companies. It is compiled by Dimensional. Dimensional sorts stocks into three profitability groups from high to low. Each group represents one-third of the market capitalization. Similarly, stocks are sorted into three relative price groups. The intersections of the three profitability groups and the three relative price groups yield nine subgroups formed on profitability and relative price. The index represents the average return of the three low-profitability subgroups. It is rebalanced twice per year. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Source: CRSP and Compustat.

Dimensional International Small Cap Index was created by Dimensional in April 2008 and is compiled by Dimensional. July 1981–December 1993: It Includes non-US developed securities in the bottom 10% of market capitalization in each eligible country. All securities are market capitalization weighted. Each country is capped at 50%. Rebalanced semiannually. January 1994–Present: Market-capitalization-weighted index of small company securities in the eligible markets excluding those with the lowest profitability and highest relative price within the small cap universe. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. The index monthly returns are computed as the simple average of the monthly returns of four sub-indices, each one reconstituted once a year at the end of a different quarter of the year. Prior to July 1981, the index is 50% UK and 50% Japan. The calculation methodology for the Dimensional International Small Cap Index was amended on January 1, 2014, to include profitability as a factor in selecting securities for inclusion in the index.

Fama/French US Value Research Index: Provided by Fama/French from CRSP securities data. Includes the lower 30% in price-to-book of NYSE securities (plus NYSE Amex equivalents since July 1962 and Nasdaq equivalents since 1973).

Fama/French US Growth Research Index: Provided by Fama/French from CRSP securities data. Includes the higher 30% in price-to-book of NYSE securities (plus NYSE Amex equivalents since July 1962 and Nasdaq equivalents since 1973).

Fama/French Total US Market Index: Provided by Fama/French from CRSP securities data. Includes all US operating companies trading on the NYSE, AMEX or Nasdaq NMS. Excludes ADRs, Investment Companies, Tracking Stocks, non-US incorporated companies, Closed-end funds, Certificates, Shares of Beneficial Interests and Berkshire Hathaway Inc (Permco 540).

Fama/French International Value Index: 2008–present: Provided by Fama/French from Bloomberg securities data. Simulated strategy of MSCI EAFE + Canada countries in the lower 30% price-to-book range. 1975–2007: Provided by Fama/French from MSCI securities data.

Fama/French International Growth Index: 2008–present: Provided by Fama/French from Bloomberg securities data. Simulated strategy of MSCI EAFE + Canada countries in the higher 30% price-to-book range. 1975–2007: Provided by Fama/French from MSCI securities data.

Fama/French Emerging Markets Value Index: 2009–present: Provided by Fama/French from Bloomberg securities data. Simulated strategy using IFC investable universe countries. Companies in the lower 30% price-to-book range; companies weighted by float-adjusted market cap; countries weighted by country float-adjusted market cap; rebalanced monthly. 1989–2008: Provided by Fama/French from IFC securities data. IFC data provided by International Finance Corporation.

Fama/French Emerging Markets Growth Index: 2009–present: Provided by Fama/French from Bloomberg securities data. Simulated strategy using IFC investable universe countries. Companies in the higher 30% price-to-book range; companies weighted by float-adjusted market cap; countries weighted by country float-adjusted market cap; rebalanced monthly. 1989–2008: Provided by Fama/French from IFC securities data. IFC data provided by International Finance Corporation.

The Dimensional Indices have been retrospectively calculated by Dimensional Fund Advisors LP and did not exist prior to their index inceptions dates. Accordingly, results shown during the periods prior to each Index’s index inception date do not represent actual returns of the Index. Other periods selected may have different results, including losses. Backtested index performance is hypothetical and is provided for informational purposes only to indicate historical performance had the index been calculated over the relevant time periods. Backtested performance results assume the reinvestment of dividends and capital gains.