Markets, like economies, go through up and down cycles. In fact, I was quoted in the Marin IJ over the weekend saying just this very thing. Regardless of the cycle we’re in, we believe that fear and greed are two emotions that should be kept out of your investment decisions.

Market Performance in Three Graphics

It is an easy and common investment mistake to dwell on the negatives. As we weigh the information we have, we know we can’t confidently predict how the macro picture will play out. At times, the relationship between the macro climate and security prices disconnects. When fear is high, investors avoid risk, driving up the prices of safe assets and driving down the prices of riskier assets—often to excess. The result is that riskier assets usually are bargain priced when fear is high, and vice versa.

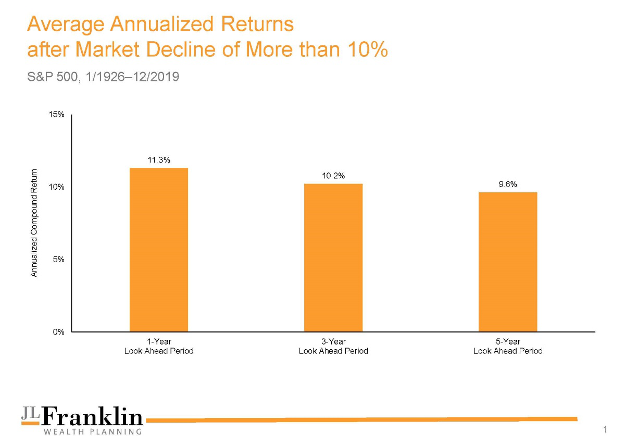

A new market high and a large market decline are not reliable indicators of future performance. The graphic below, Average Annualized Returns after Market Decline of More than 10%, shows the performance of U.S. large cap stocks over one-, three-, and five-year periods following a market decline of at least 10%. Note that every one of the periods since 1926 has had a positive return.

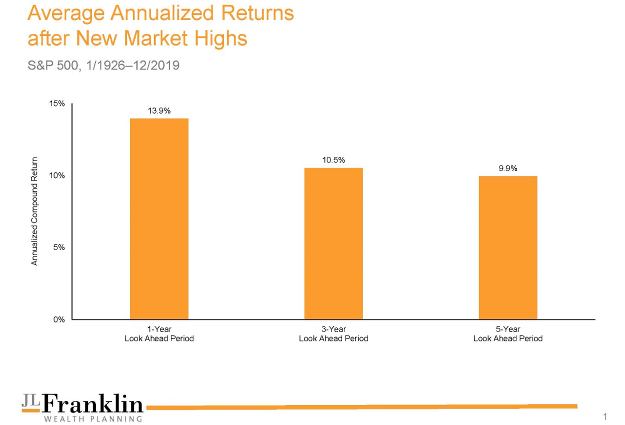

The inverse is also true. In this graphic, Average Annualized Returns after New Market Highs, since 1926, U.S. large cap stocks have had positive returns over one-, three-, and five-year periods following a new market high.

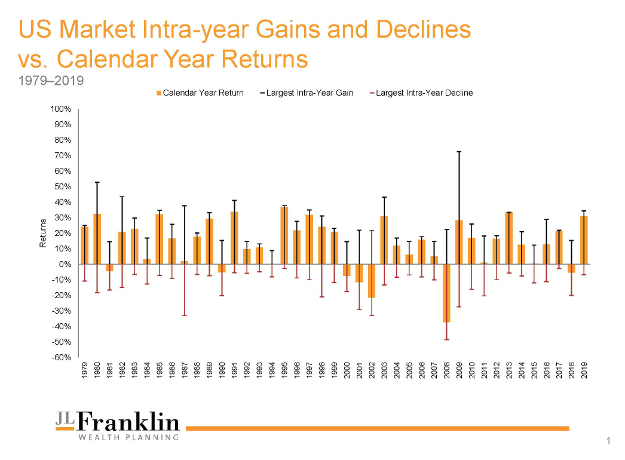

The performance of the stock market can vary wildly within any given year. In fact, such volatility is normal. The graphic below, U.S. Market Intra-Year Gains and Declines vs. Calendar Year Returns displays returns of the Russell 3000 Index for the past 40 years, since 1979. Each orange bar represents the calendar year return. The red and black whiskers show the largest gain and decline within each year.

Even in years with high calendar-year returns, a large intra-year decline may have occurred. A long-term focus can help block out the noise.

10 Investment Truths

The daily ride of the stock market can feel destabilizing if you focus on it too closely. But if you keep in mind that these extreme ups and downs will pass, stay focused on your long-term investment goals, and keep your emotions in check, the volatility can be a lot easier to stomach.

Below are 10 investment truths that may help you stay focused on the long term.

- The fundamental investment risk is not losing one’s money, but outliving it. Risk isn’t loss of principal. It’s the extinction of your purchasing power while you’re still alive.

- The only safety lies in the accretion of purchasing power. Accumulation of purchasing power is a positive investment return, net of inflation and taxes.

- The great long-term risk of stocks is not owning them. During tough economic times, risk premiums rise to compensate investors. While volatility can be hard to stomach, there’s no evidence that it is a leading indicator of future negative returns.

- Everything you need to know about the movement of stock prices can be summed up in eight words: The downs are temporary, the ups are permanent. Stock prices go down approximately 25% every five years or so. You can only create a permanent loss by panicking and selling out.

- When we are experiencing a bear market, think “big sale.” When prices are down, you are buying low, so stock up!

- Managed portfolios of stocks are better than individual stocks. You can break one pencil; 50 pencils tied together are hard to break, and this is diversification.

- Dollar cost averaging is a conservative way to enter the market. Each time you add to your investments, you’re buying new shares that track precisely to the current market price.

- Learn to love volatility. Working with us protects your long-term well-being, since JLFranklin Wealth Planning is impervious to panic. In an efficient market, higher volatility means higher returns.

- Don’t be afraid of being in the next 25% downtick. DO be afraid of missing the next 100% uptick. Stay fully invested all the time; don’t try to time the market.

- Prior to retirement, people should own as close to 100% equities as they can emotionally stand. Then, after retirement, they should own as close to 100% equities as they can emotionally stand. Cash for short-term needs should be carved out of your portfolio and placed in a cash reserve account.

Adapted from The Excellent Investment Advisor, by Nick Murray

If you have any questions about your portfolio or your financial plan, please reach out.